A self-assessment of my blockchain bets in 2019 — did I hit or miss?

Time to score my predictions.. (Photo by Jorge Franganillo on Unsplash)

Everyone in the crypto space seems busy right now publishing their predictions for 2020. Yet while Twitter abounds with a variety of divination, some interesting and thoughtful, but also some delusional and naive (Sorry #XRPArmy, but $1,000 XRP would value the asset at more than half of global GDP — not gonna happen), I notice that few people actually review their predictions from last year. Self-assessment and public disclosure is low, kinda like how your friend who plays poker online loves talking about their winnings but keeps silent about the losses.

So, in the decentralised spirit of transparency I’m going to take a minute to look back to my predictions for 2019 and critically appraise how I did. Any comments or disagreements more than welcome!

Brief Recap of 2019 Predictions

In December 2018 I summarised my predictions for 2019 as the themes hereunder:

Securitizing tokens and tokenizing securities

Institutional involvement in the cryptocurrency market

The halo effect of industries being built around blockchain

The future of stablecoins

The rise of Proof of Stake

I’ll need to revisit some written excerpts in order to appraise these since they aren’t so specific (note to self: clearer statements next time). Quoted in line below.

Theme 1 : Securitizing tokens and tokenizing securities

(Prediction Result: Partial Hit)

I was right about the regulatory clarity and new ground-up security token exchanges, but not so right on the other points.

(Full text here.)

A key part of this trend will be the increasing prevalence of security tokens.

Based on all the activity in the security token industry this year, I think I can stand behind this claim, however if I’m critical of myself this statement is too generic to be worth much. In general the year definitely didn’t live up to the STO hype for some, although there still some notable developments and announcements.

In the first half on 2019, the number of STOs grew 16% to 57 vs. 49 during the same period in 2018, while the number of ICOs fell 74% to 403 from 1570 (Source: inwara)

we would expect to see an increasing willingness of institutions and issuers to take existing securities and ‘wrap them’ in a blockchain-based token.

Facing the limitations of the crowdfunding model, companies have begun pivoting from helping companies issue security tokens to helping them tokenize existing securities (Harbor being a notable example).

Elsewhere, some traction here but less than I expected. One highlight was China’s 20 billion yuan ($2.8bn) issuance of blockchain-based bonds in December. Several other startups have had their equity tokenized. But success has been muted in the real-estate sector. A number of publicized deals failed to come to fruition (like this one) as institutional interest failed to materialise on the demand side.

for the newer and more cutting-edge blockchain projects, we will see increasing clarity from regulators as to what constitutes a so-called ‘security token’ and under which rules they should/will be regulated.

Although many regulators are still adopting a wait-and-see approach, we did see plenty of good progress as security tokens continued to gain credibility from regulators and other entities in this space. For example, the UK’s Financial Conduct Authority (FCA) published guidance clarifying that security tokens do indeed fall under it’s regulatory scope, Germany’s BaFin approving a number of STOs (including those by Bitbond and Fundament), and the U.S. Securities and Exchange Commission (SEC) approving two Reg A+ token offerings (Blockstack and the Props Project).

I predict more exchanges will appear that are built from the ground up as explicit security-token exchanges, with all the regulatory measures and controls that will entail.

These ground-up security token exchanges are appearing (e.g. Templum, OpenFinanceNetwork, 1exchange), but are facing increased competition from incumbents (Coinbase, Binance) or traditional stock exchanges (SIX in Switzerland, or LSE in UK). Many start-ups are still quite some way from launching an actual secondary-market ‘exchange’ (probably because this is hard!) and either pivoting / narrowing their scope to just primary-market issuance.

The legal ‘grey area’ in which many unlicensed exchanges are still happily (and profitably!) operating will continue to shrink.

The grey area shrunk less than I expected actually. There are still hundreds of exchanges out there that enjoy operating with lack of definitive regulatory clarity. Watch out for AMLD5 / FATF developments unfurling in 2020 though, as well as more statements coming from regional banks and regulators…

Theme 2: Institutional involvement in the cryptocurrency market

(Prediction Result: Miss)

I expected more crypto investments coming from traditional players, which didn’t materialise.

(Full text here.)

Now that it’s clear that crypto is here to stay, we will increasingly see larger pools of money beginning to get involved.

I’m surprised there wasn’t more public announcements of institutional bitcoin investments this year. It seems that the euphoric frothy ICO boom and bust caused some lasting damage to the industries reputation in the eyes of traditional institutions. Big banks and funds are staying away from the investment side, and most private bankers and family office investment chiefs that I speak to say they aren’t quite ready to dip their toes in yet, as if they are all waiting to follow someone else’s lead. There’s for sure plenty of institutional money that was accumulating bitcoin in 2019, but it was largely taking place independently or via special purpose funds or vehicles with a looser investment mandate.

The arrival of ever-more instruments such as futures, ETFs, Security Tokens, and even fixed-income crypto-securities will accelerate this trend.

Bitcoin futures were here already, with the notable new launch of Bakkt by the Intercontinental Exchange (ICE), joining existing futures products from the CME and other crypto-exchanges, even while CBOE abandoned bitcoin futures this year. ETFs are still stubbornly absent after the SEC’s repeated denial of ETF proposals including most lately one from Bitwise.

Theme 3: The halo effect of industries being built around blockchain

(Prediction Result: Partial Hit)

There are many examples to back up this claim, but I’m docking myself the generic statement.

(Full text here.)

In the short term, we can expect to see emerging industries directly sprouting from existing ones

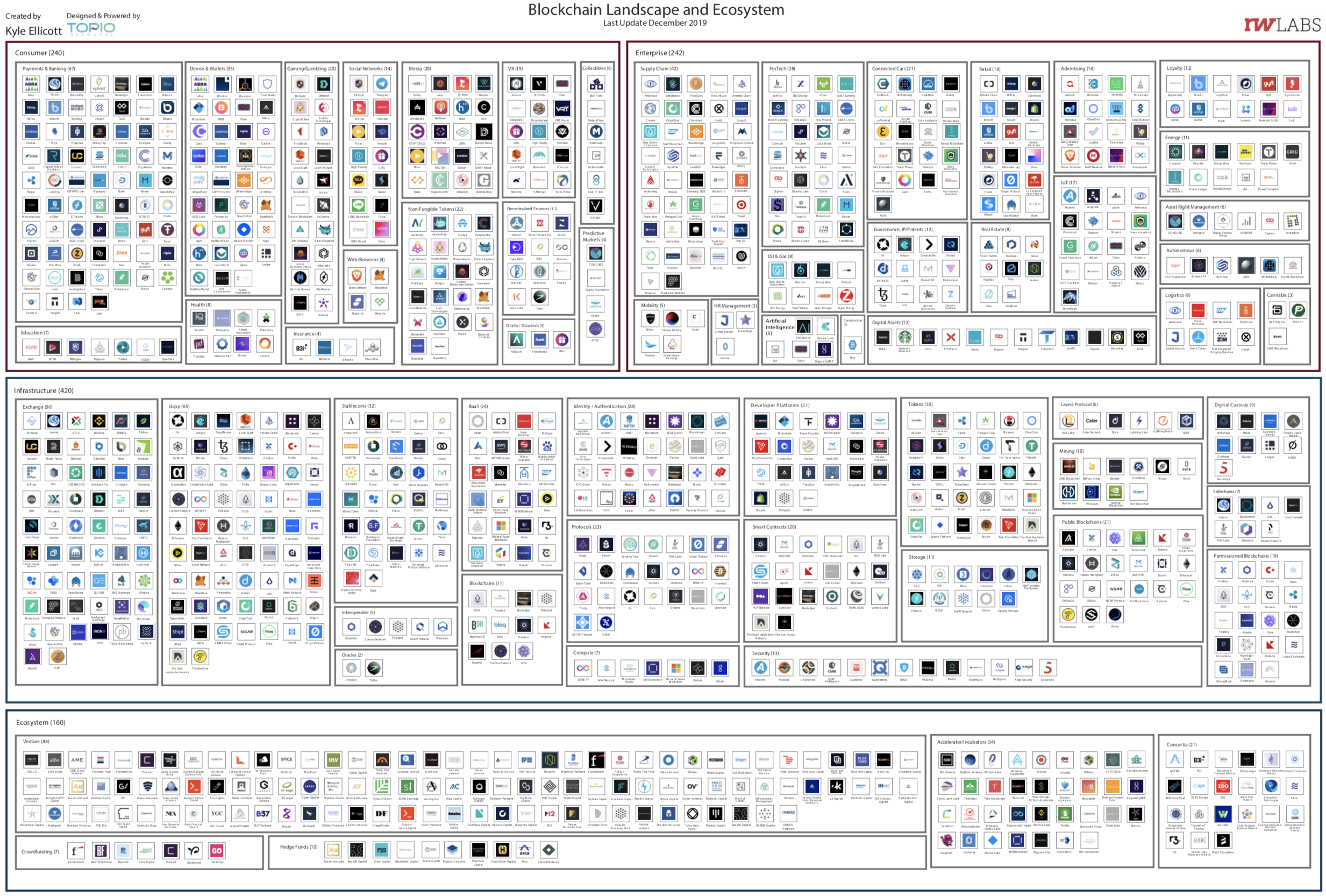

I’m going to partially disqualify myself here because it’s too easy to confirm something so general. However, it’s certainly true that the crypto / blockchain ecosystem is quickly becoming a sprawling landscape. The excellent diagram below shows some scale of this, and while many of these companies and projects are still somehow related to the underlying industry infrastructure buildout, there are still some good examples of completely new business models emerging from that infrastructure. To pick some of examples:

Smart Contracts Infrastructure → Professional Contract Security Tools (e.g MythX)

Crypto Custody Infrastructure → Compounding Crypto Interest Accounts and lending (e.g. BlockFi)

Staking-As-A-Service Infrastructure → Independent Payout Auditors (e.g. BakingBad)

Decentralised Finance Infrastructure → Asset management tools (e.g. Zerion)

These completely new blockchain-native applications come in addition to continuing development in many core areas such as custody, insurance, lending, and exchange.

Credit : Kyle Ellicott (Full Res Download here)

Theme 4: The future of stablecoins

(Prediction Result: Hit)

This year saw a big increase in stablecoin growth and innovation.

(Full text here.)

Whilst Stablecoins aren’t a brand-new addition to the Crypto ecosystem, I do predict they’ll solidify their place in the market in 2019.

Stablecoins have continued to pour onto the markets, confirming real demand. A Binance report from November 2019 indicated that 96% of institutions surveyed were using stablecoins, predominantly fiat-backed. Although many stablecoins are straightforward fiat-collaterized variants of the original stablecoin, Tether, there has also begun a number of new projects that innovate on different types of stablecoin, including crypto-backed, asset-backed, non-collateralized (aka algorithmic) stablecoins, and all sorts of hybrids. Notable launches include Saga (December) and Multi-Collateral Dai (November).These categories all come with different pros and cons around stability [sic], reserves risk, liquidity, trust, and so forth. We’ve even started seeing ‘stablecoins-of-stablecoins’ with projects such as USDx using a basket of other stable coins including USDC, TUSD, PAX and DAI.

Binance Research — Institutional Market Insights — 2nd edition

Of course the big story of the year was Facebook’s Libra stablecoin (announced June), which raced digital currencies to the top of the agenda for many governments, given Facebook’s international reach. Furthermore, Central Banks all around the world seem to be discussing, announcing and working on stablecoins of their own, so-called CBDCs (Central Bank Digital Currencies).

See my 2020 predictions for more on Libra and CBDCs.

Theme 5: The rise of Proof-of-Stake

(Prediction Result: Hit)

PoS has caught on fire in 2019, with staking rewards being all the rage

(Full text here.)

My expectation is that as people begin to understand and experience investment yield in crypto, this will spark a new wave of interest in Proof of Stake blockchains, with main beneficiaries being the newer generation PoS projects […]

I wrote about this in more detail earlier this year, after predicting that staking rewards would start garnering more popularity for Proof-of-Stake (PoS) blockchains in 2019.

Plenty of evidence shows this to be the case. This year we have seen the launch of dedicated staking support by major exchanges like Coinbase Custody (March), Coinbase retail (November), Binance (September), and Kraken (December); the launch of Cardano’s Incentivised Testnet ‘Shelley’ (December), the seed-funding and rapid growth of institutional PoS services platforms like Staked (January), and many other Staking-As-A-Service companies popping up.

Meanwhile, popular PoS cryptocurrencies like Tezos, Cosmos, Decred, and Cardano were busy being listed on an ever-greater number of large exchanges, large numbers of staking / delegate pools and associated tools sprung up, and a huge wave of articles and explainers appeared online as people started waking up to the appeal of earning compounding, non-custodial, realtime, fiat-busting yields denominated in crypto.

According to Staked, ~25% of the total cryptocurrency market uses PoS as a security model at the end of 2019 (up from ~10% at the beginning of the year according to my estimates). When (if?) Ethereum eventually switches to PoS that number will be greater still. However, while it’s clear that PoS is on the rise, I also think that the drawbacks of this security model are not being discussed enough and, I actually also believe we will see a sort of renaissance for Proof-of-Work blockchains in the future.

So that’s it for 2019. Two hits, two partial hits, and a miss. I hope the above also served as a useful recap / cross-section of what happened in crypto in 2019. It’s hard to believe that I only wrote these a year ago! This space moves so fast, and I don’t expect that to slow down any time soon.

Roll on 2020!

Andy

January 2020